Background:

India's startup environment is a breeding ground for innovation and growth, luring companies to return home. The once-common practice of ‘flipping’ - where companies incorporated their operations abroad to tap into specific benefits - is giving way to a phenomenon known as ‘reverse flipping’ or ‘internalization.’ This reversal involves Indian companies, initially established overseas, strategically repatriating their legal headquarters back to their home soil. Notable examples of successful internalisation include companies like PhonePe, Groww, and Pepperfry, with companies such as Razorpay, PineLabs, Meesho, UrbanLadder, Livspace and Zepto in various stages of homecoming.

The trend of reverse flipping has been fuelled by better valuation in Indian markets, support from the Indian Government, simplified regulatory compliances and easy access to capital. Further, the IPO market in India has shown resilience and growth, providing a viable exit strategy for investors looking to realize their returns. In this article, we have examined few structures for achieving a ‘reverse flip’ and the attendant implications from exchange control and taxation perspective.

Structuring the flip:

Choosing the right structure for a reverse flip is critical, as it impacts legal, regulatory, and tax considerations. Here, we have delved into two ways of doing this: ‘Inbound Merger’ and ‘Share Swap Arrangement’.

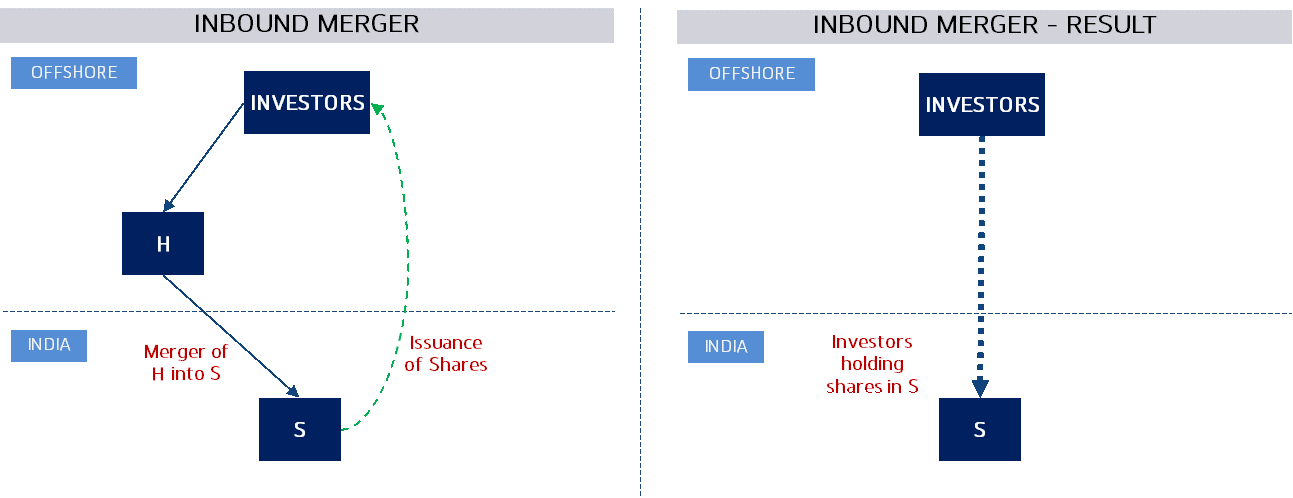

1. Inbound Merger

Under this, the Foreign Holding Company (‘H Co.’) which holds 100% shares in the Indian Co. (‘S Co.’), would merge with and into S Co. Further, the non-resident shareholders of the H Co. would receive the shares of S Co. The diagrammatic representation of this structure and the regulatory and tax considerations thereof have been discussed below:

(a) Companies law

1. Section 234 of the Companies Act, 2013 (‘Companies Act’) read with Rule 25A(1) and (3) of the Companies (Compromises, Arrangements and Amalgamations) Rules 2016 (‘Rules’) contains provisions relating to cross-border mergers i.e., between an Indian company and a foreign company.

2. These provisions inter-alia provide that firstly, RBI approval is required for an inbound merger. Secondly, S Co. shall obtain a valuation report from a registered valuer, with a valuation in accordance with the internationally accepted principles of valuation.

3. Thereafter, S Co. shall file an application for approval of the inbound merger with the National Company Law Tribunal (‘Tribunal’) which shall be subject to meeting of members and creditors of S Co. and objections from the statutory authorities. Though this process is clean, it may approximately take 7-9 months.

(b) Foreign Exchange law

1. The Foreign Exchange Management (Cross Border Merger) Regulations, 2018 (‘Merger Regulations’) inter-alia provides for detailed aspect of an inbound merger from exchange control perspective.

2. The issuance of securities by S Co. to the shareholders of H Co. shall be subject to pricing guidelines, entry routes, sectoral caps and other attendant conditionalities as provided under the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (‘NDI Rules’).

3. Further, outstanding guarantees and borrowings of H Co. from overseas sources which would become the borrowing of the S Co. are required to comply (i.e., within a period of 2 years from such transfer) with the ‘External Commercial Borrowing’ norms and the Foreign Exchange Management (Borrowing and Lending) Regulations, 2018, except the requirement on end use restrictions.

4. If any asset or security outside India (not permitted to be held or acquired by an Indian resident) is brought on the books of S Co., then such assets are required to be sold within a period of 2 years from the date of sanction of the scheme by the Tribunal. The sale proceeds should be repatriated to India immediately or used to set off any overseas liability which is not permitted to be held by the S Co.

5. The requirement of taking specific RBI approval under the Rules shall not be required if the cross-border merger is in accordance with the Merger Regulations and a certificate to that effect is furnished by the Managing Director / Whole Time Director and Company Secretary of the concerned companies.

6. Further, companies involved in such merger are required to ensure that any regulatory actions related to non-compliance, contravention or violation of foreign exchange laws are completed. This would entail regularising and compounding the foreign exchange violations prior to commencing the inbound merger.

7. Laws of the country of residence of the foreign company need to be separately examined

(c) Income-tax law

1. The transfer of capital assets from the H Co. to S Co. as well transfer of shares by the non-resident shareholders in lieu of shares in S Co. are not taxable as capital gains under Section 47(vi) and 47(vii) of the Income Tax Act, 1961 (‘ITA’). However, such amalgamation must meet the conditions specified in Section 2(1B) of the ITA. If these conditions are not fulfilled, then, in the hands of the H Co. as well as its shareholders, the transactions would be subject to capital gains tax in India, unless the relevant tax treaties provide taxing rights only to the country of residence of H Co. or its shareholders.

2. Further, the tax losses of the H Co. would become the loss of S Co., subject to conditions of Section 72A of the ITA. If H Co. is engaged in a trading business or service business, then it would not amount to ‘industrial undertaking’ under section 72A(7)(aa) of the ITA and hence, S Co. may not be able to absorb the tax losses.

3. A change in the shareholding of S Co., where shareholders beneficially holding at least 51% of the voting power prior to the merger do not continue to hold the same voting power post-merger, may invite lapse of brought forward tax losses of S Co. under Section 79 of the ITA. However, there is judicial divergence with respect to the test of beneficial holding of 51% of voting power i.e., whether the change is to be seen qua ultimate beneficial owner[1] of shares or the direct shareholding[2]. Section 79 of the ITA is however, inapplicable to startups recognized by the Government of India.

(d) Further, the tax implications in the country of residence of the foreign entity would need to be analysed separately.

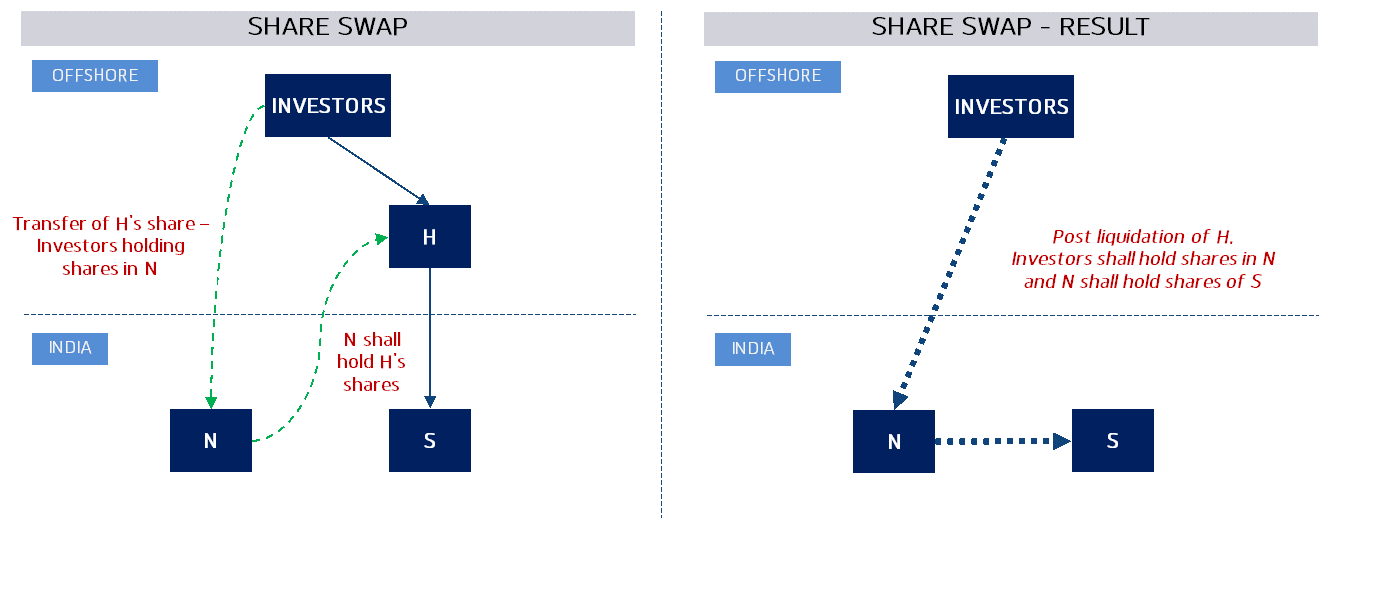

2. Share Swap

Under the share swap method, firstly, the foreign company’s shareholders will exchange their shareholding in H Co. for the shares of a new Indian company (‘N Co.’) and consequently, N Co. would hold shares in H Co. Resultantly, the shareholders would directly hold shares of N Co. and N Co. would become the holding company of H Co. Secondly, H Co. would be liquidated as per the laws of its country and its assets (being shares of S Co.) would be distributed to shareholders of N Co. Consequently, N Co. would hold shares of S Co. The diagrammatic representation of this structure and the regulatory and tax considerations thereof have been discussed below:

(a) Foreign Exchange law

An Indian company (engaged in automatic route sector) is permitted to issue equity instruments to a person resident outside India against swap of equity instruments. Acquisition of shares of N Co. by a non-resident will attract the NDI Rules which inter alia, provide restrictions as to the permitted business sectors, entry routes and sectoral caps. It may also trigger approval requirement from different regulators depending upon the nature of business. The resultant structure as depicted above would also require an analysis of relevant ‘Downstream Investments’ regulations.

Acquisition of shares by the N Co. in H Co. shall be governed by the Foreign Exchange Management (Overseas Investment) Rules, 2022 which permits overseas investment by way of swap of securities.

The equity capital should be valued at an arm’s length basis taking into consideration internationally accepted pricing methodology.

(b) Income-tax law

1. The swapping of shares of H Co. for shares of N Co. would be regarded as ‘exchange’ and hence, a ‘transfer’ under Section 2(47)(i) of the ITA.

2. The foreign shareholders would be liable to capital gain taxation in India under Section 9(1) of the ITA, on transfer of shares of H Co. if such shares derive their value, directly or indirectly, from assets located in India, unless the relevant tax treaties provide taxing rights only to the resident country of these investors. The taxable gains would be the delta between the value of the shares of N Co. and H Co. on the date of such swap, subject to fair valuation of shares.

3. As discussed supra, the change in shareholding of S Co. may impact its right to carry forward and set off of losses under Section 79 of the ITA, subject to the contention of ultimate beneficial ownership v. direct shareholding.

4. In the hands of the H Co., the transfer of shares of S Co. to N Co. would not be taxable as capital gains in India under Section 46(1) of the ITA. In the hands of N Co., the market value of these shares as on date of distribution, would be taxable under ITA. The portion up to the accumulated profits of H Co. would be taxable as ‘deemed dividend’ under Section 2(22)(c) of the ITA. The portion exceeding such accumulated profits would be taxable as capital gains under Section 46(2) of the ITA. This distribution may require reporting under transfer pricing laws in India.

(c) The reporting requirements, dissolution of H Co., eligibility of a company for getting its shares listed on an Indian exchange and tax implications in the country of residence of H Co. require separate examination.

3. Alternative options

Alternative structures could be explored to suit the objectives of investors and in view of regulations of jurisdictions. These include, amongst others, (i) a capital reduction exercise to be undertaken by the foreign company and transferring shares of the Indian subsidiary company as consideration to the investors; (ii) setting up a new cash-rich company in India which could directly acquire the foreign company’s shares.

Another attractive proposition is to establish legal base within the Gujarat International Finance Tec-City (GIFT IFSC). This offers a unique advantage – companies can leverage the benefits of a reverse flip while simultaneously accessing the specialized regulatory framework and tax incentives designed for international financial services within GIFT IFSC. However, navigating the complexities of establishing a presence in GIFT IFSC along with attendant regulatory compliance requires careful consideration. The upcoming Union Budget is expected to bring some regulatory relaxations and benefits for foreign domiciled Indian startups to relocate their business to GIFT IFSC.

4. Other considerations and way forward

Compliance with DPIIT’s Press Note 3 might also be required if the investing entity or its beneficial owner is based out of a land border sharing country with India. At the same time, it is also imperative to examine the stamp duty implication on such transactions. Reverse flips can also complicate employee stock option plans (ESOPs) by potentially forcing employees to wait for a minimum period of one year to exercise their options due to Indian regulatory requirements. Novation of existing contracts might also pose a hurdle, requiring review of contracts and negotiations with the concerned parties.

Companies undertaking a reverse flip must carefully consider such challenges and develop strategies to mitigate them, ensuring a smooth regulatory transition in a tax efficient manner.

[The first and second authors are Associate Partner and Principal Associate, respectively, in Direct Tax practice, while the third author is a Principal Associate in Corporate and M&A practice at Lakshmikumaran & Sridharan Attorneys]

[1] CIT v. AMCO Power Systems Ltd. [2015] 235 Taxman 521 (Kar.); CLP Power India (P.) Ltd. v. DCIT [2018] 170 ITD 744 (Ahmedabad – Trib.); Hiranandani Healthcare (P.) Ltd. v. CIT(A)/NFAC [2023] 157 taxmann.com 551 (Mumbai - Trib.)

[2] Yum Restaurants (India) (P.) Ltd. v. ITO - [2018] 380 ITR 637